UK & Ireland Reclaim EMEA Top Spot In M&A Activity

Data collected by Mergermarket and analysed by Datasite, shows that the UK & Ireland region is back in first position within the larger EMEA (Europe, Middle East & Africa) market in terms of companies exiting via M&A deals.

After a sub-par performance in the first half of 2024, more companies in the UK & Ireland region have been the potential target of mergers and acquisitions, according to the Deal Drivers Q3 2024 Report published by Datasite.

This data is particularly timely because it tracks “companies for sale” according to Mergermarket data, which includes companies that are currently part of potential M&A deals, and therefore doesn’t rely on historical, disclosed M&A data which is often delayed by a few months.

Q1 and Q2 2024: UK & Ireland Lagging Behind

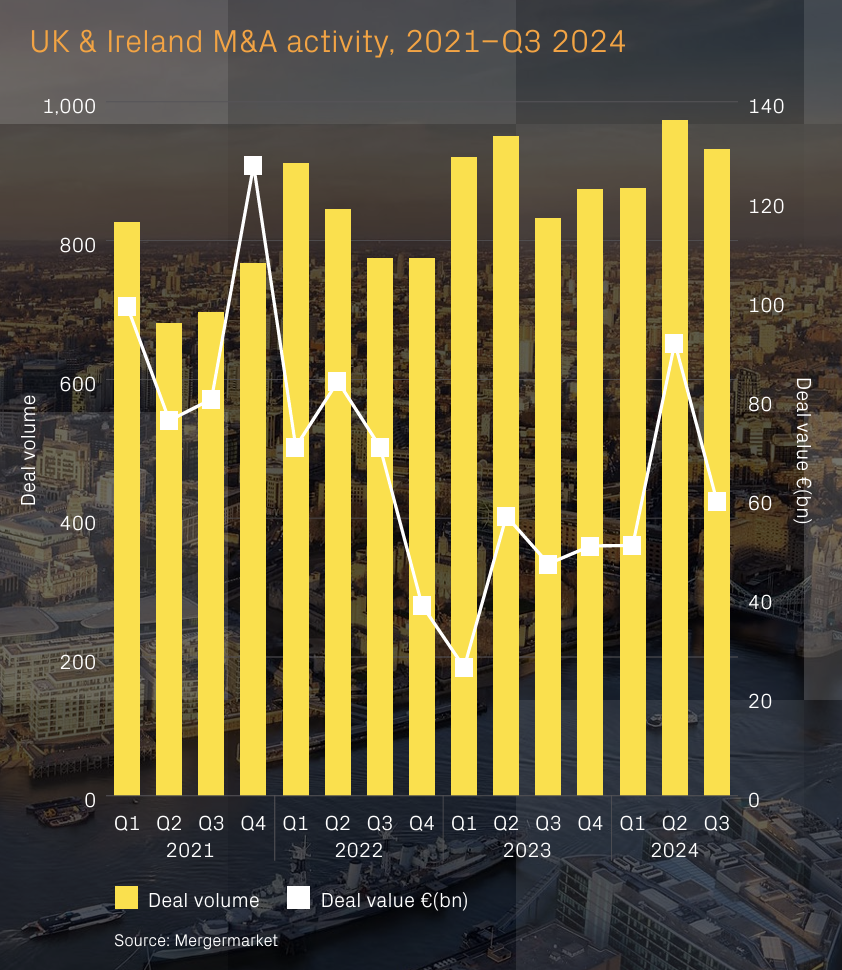

In the first half of the year Mergermarket only reported 305 deals in the making in the British & Irish region—although that did include the largest M&A deal in Europe this year: Intel’s part sale of their Fab 34 venture to Apollo for just under £10bn. Other EMEA geographies including DACH, Central/Southern Eastern Europe and the Middle East recorded higher number of deals being made in H1 2024.

Germany, Austria and Switzerland absolutely dominated the Industrials & Chemicals sector, while CEE/SEE and Turkey, Middle East & Africa led the TMT (Technology, Media and Telecommunications) space.

Datasite attributes the sluggishness of the UK market compared to the rest of EMEA during this period to Government uncertainties at a time when Rishi Sunak was about to call an election. It also notes, however, that the interventionist policies of the Labour Government towards cross-border M&A run the risk of deterring international buyers.

Q3 2024: Britain back on top

This past quarter’s report was much more encouraging, in particular for the UK tech scene which, according to Dealroom data cited in the paper, show that capital raised by UK tech sector start-ups and scale-ups represents nearly one third of all venture capital raised across Europe this year.

UK & Ireland led the EMEA pack in the TMT, Consumer and Business Services sectors, totalling 326 ongoing deals in Q3 2024 according to Mergermarket’s “companies for sales” data.

A large portion of UK mergers and acquisitions was made possible by a cash influx from overseas, with US bidders accounting for €21.8bn worth of M&A in Q3, or 37% of total investment. According to Datasite, American acquirers “see tremendous value in this market, benefiting from relatively lower-entry multiples for quality assets.”

In terms of deals announced, UK & Ireland look like they’re on a positive trend in terms of deal volume, as they have been for a few years—save a few ups-and-downs. Deal value, on the other hand, is yet to return to its 2021 highs, and while Intel and Apollo’s £9.9bn joint venture announced in may helped bring the metric close to €100bn in Q2, the overall trend seems to speak of much slower growth.

While mega-deals might be back in vogue in the US, now with the added confidence of the Republican government’s hands-off approach to M&A, the UK funding environments still revolves around smaller checks and more conservative valuations.

The information available on this page is of a general nature and is not intended to provide specific advice to any individuals or entities. We work hard to ensure this information is accurate at the time of publishing, although there is no guarantee that such information is accurate at the time you read this. We recommend individuals and companies seek professional advice on their circumstances and matters.

-

Lessons From The UK’s Top 50 Exits

12 November 2025

The most successful founders are those who build a company to be bought, not sold.

Report : Exit and Trends

-

The Jaguar Land Rover Cyber Attack: a £1.9bn Case Study in Systemic Risk

23 October 2025

The Jaguar Land Rover attack highlights several major threats and vulnerabilities in the cybersecurity space.

Report : Strategy and Trends

-

Green Energy & Renewables: 2025 Valuation Multiples

1 May 2025

Trump’s victory dealt the final blow to the Green Energy sector at the end of last year. In Q4 2024 the median EV/Revenue multiple was 5.7x.

Report : Tech, Trends and Valuation

Sign up for the Founder's Bulletin

Join our community of 4,000 + Founders, Entrepreneurs & Advisors. Refreshingly simple financial insights to help your business soar.