Autotech & Mobility: 2024 Valuation Multiples

If you bought a car in the UK in the past couple of years, chances are it was an electric or a hybrid vehicle. This means it was equipped with all sorts high-tech hardware and software. We collectively refer to all these pieces of innovative equipment as Autotech.

The thing about Autotech is that any of such components—that today are considered fundamental to a brand new car—have been conceived, developed and produced no more than two decades ago. That may seem like a lot, but not if you think that combustion engine cars are almost 140-years old. In that time, despite incredible progress and improvements, the key principles and components of a car have remained largely the same. That was until we came up with:

- batteries efficient enough to spin the wheels of a full-sized car over useful distances,

- computers powerful enough to run the car’s core systems digitally,

- the infrastructure to build, deliver, manage and maintain these expensive drive-able computers.

The key drivers of the huge transformation this market has seen are certainly electrification and digitisation. These two movements, led by a global effort to combat climate change on the one hand, and from wider user-experience trends on the other, were embodied first and foremost by electric car manufacturer Tesla—the largest car company by market cap at the time of writing, although not even in the top 10 by sales—which pioneered the “smartphone-on-wheels” design that made electric vehicles (EVs) rise to prominence.

Tesla didn’t just change the way cars are made, but also the way they are sold and maintained and the way they operate. With a fully D2C approach, Tesla’s sales process mostly takes place online, drastically reducing the cost of sale per vehicle. They began selling optionals on a subscription-basis as well as delivering over-the-air software updates to carry out safety checks, maintenance and to manage recalls for which traditional automakers would require physical fixes. They were also front-runners, together with independent players such as Waymo and Baidu, of self-driving technology, promising the ultimate revolution in the industry by removing the need for a human driver.

All these extremely R&D-intensive innovations led the way for hundreds of start-ups and scale-ups looking to develop each individual component that makes this huge industry shift possible: software to optimise range, assist driving, deliver updates and manage sales, as well as hardware to gather sensor data, increase battery capacity and efficiency, and provide charging points.

As traditional automakers realised they had to keep up with the disruptors, many of them adopted aggressive M&A strategies to acquire or partner with up-and-coming Autotech companies to integrate their cutting-edge technologies into their smart vehicles.

M&A Consultancy firm Hampleton Partners released their latest Autotech & Mobility Report, providing an in-depth analysis of the most recent M&A and valuations trends in the space.

Firstly, Hampleton Partners found that the first half of 2023, with 68 announced deals, about 10% shy of the all-time-high for M&A volume. 40 of these deals involved companies going public via SPAC, proving it is still a sector-favourite exit route.

Trailing 30 month EV/Revenue multiples for the Autotech sector showed a median of 3.4x in H1 2024, a 4-year high. Values within the 68 announced deals were pretty evenly distributed between 1.8x to 5.4x, a much more consistent distribution than in previous years, showing growing consensus on how companies in the sector are valued.

In terms of geography, North America is still home to over half of the acquisition targets from last year. European companies accounted for 37% of Autotech acquisition targets, being sought primarily by European acquirers, showing an increase in M&A consolidation in Europe.

However, Hampleton’s research also shows how the Chinese market has claimed the undisputed top spot for both manufacturing and sales of Battery Electric Vehicles. It is estimated that in 2022 Chinese companies sold more than double the BEVs than American and European manufacturers combined, and that all newly sold Electric cars in Europe will eventually be Chinese-made, irrespective of their manufacturer.

Finally, the report mentions the likes of Qualcomm—the US-based semiconductor giant which has made some significant Autotech acquisitions over the past years—overtaking Apple and Android based systems as the provider of software for electric vehicles. In the meantime, the push towards autonomous driving makes slow but steady process, even in the UK, while Tesla’s supercharging infrastructure became the North American standard, with more and more of its competitors joining their Charging Network.

The information available on this page is of a general nature and is not intended to provide specific advice to any individuals or entities. We work hard to ensure this information is accurate at the time of publishing, although there is no guarantee that such information is accurate at the time you read this. We recommend individuals and companies seek professional advice on their circumstances and matters.

-

Lessons From The UK’s Top 50 Exits

12 November 2025

The most successful founders are those who build a company to be bought, not sold.

Report : Exit and Trends

-

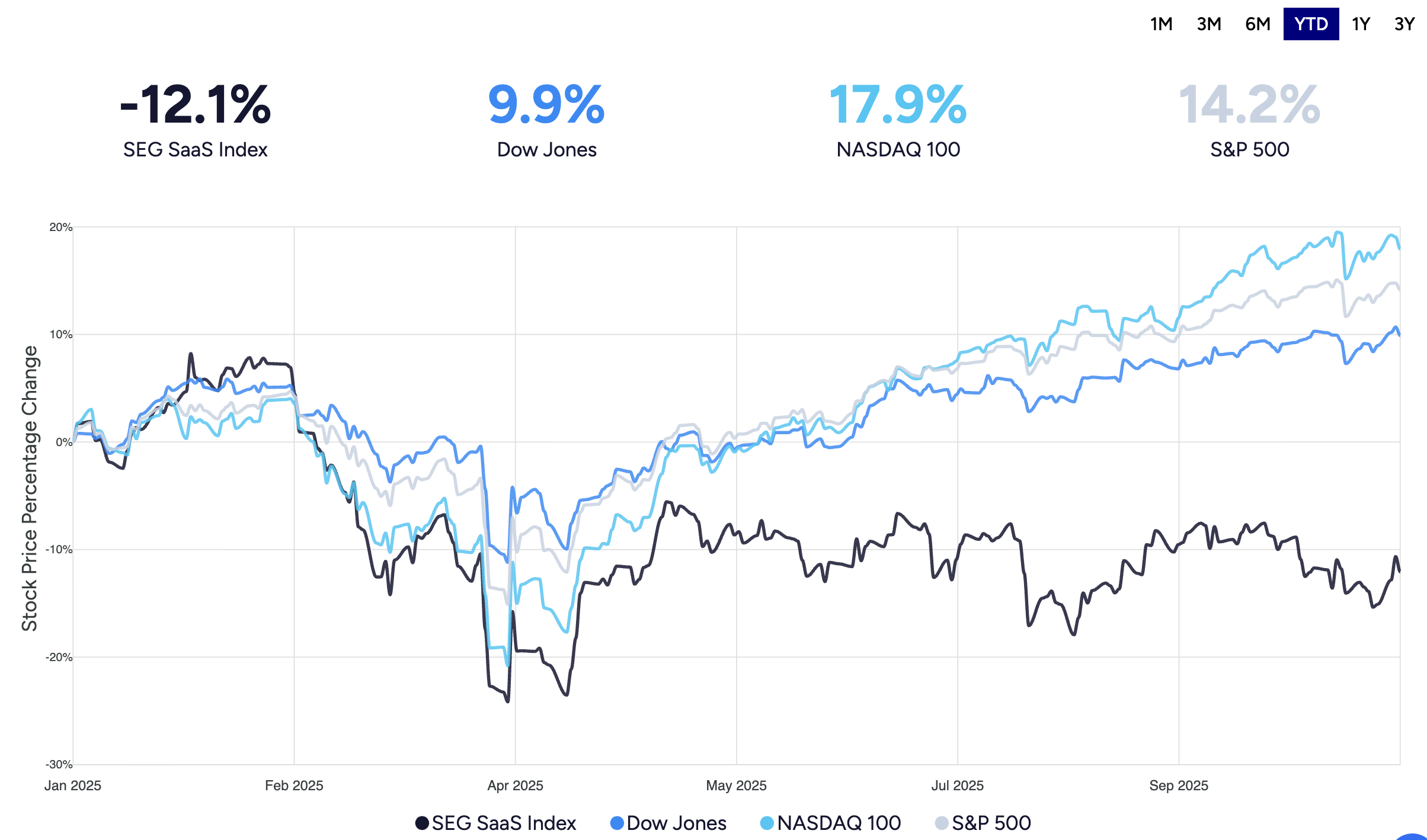

SaaS Stumbles in 2025: End of an Era, or Just Growing Pains?

23 October 2025

There is a widening gap between SaaS and the rest of the market starting in April 2025, and it’s just getting larger and larger.

Report : Tech and Valuation

-

The Jaguar Land Rover Cyber Attack: a £1.9bn Case Study in Systemic Risk

23 October 2025

The Jaguar Land Rover attack highlights several major threats and vulnerabilities in the cybersecurity space.

Report : Strategy and Trends

Sign up for the Founder's Bulletin

Join our community of 4,000 + Founders, Entrepreneurs & Advisors. Refreshingly simple financial insights to help your business soar.