Health & Wellness: 2024 Valuation Multiples

Although health and wellness have always been central to human societies and economies, their exact definition has changed massively over time according to the values, priorities and habits of the time. Ever since the pandemic, health and wellness started to become synonyms with home workouts, mindfulness, circadian rhythms and many other concepts that were not necessarily considered part of a healthy lifestyle before.

Today, wellness goes beyond personal priorities: Bloomberg reports that the sector raked in $5.6tn in revenue in 2022, and that’s projected to grow to $8.5tn by 2027. For context, that’s twice the GDP of some G7 countries.

Once limited to sports equipment and clothing brands, the wellness sector has now expanded into a myriad of segments, with sometimes blurred lines and lots of overlap. Tech-based categories such as Fitness-as-a-Service (think Peloton), TeleHealth apps for mindfulness and mental health and wearable health trackers have been on the rise in the past few years, boosted by the global pandemic.

At the same time, established companies in adjacent sectors have entered the wellness market from multiple sides, like food and beverages, skincare brands, sexual health products and more, benefitting from a widened definition of “wellness” in the consumer’s eyes.

A busy and steady M&A environment underlines this sector’s consolidation. After peaking in the first half of 2023, the mergers and acquisition deal volume has slightly cooled, however the first quarter of 2024 still showed some impressive activity like the $380m acquisition of eco-friendly feminine care brand Honey Pot by Compass Diversified Holdings.

While some deals are part of proven diversification strategies by FMCG giants like Unilever, P&G or Mondelez, Others reflect strategic moves from wellness companies seeking to enters adjacent subsectors, such as athletic clothing brand Lululemon acquiring Peloton competitor Mirror for $500m.

The Global X Health & Wellness ETF (BFIT), managed by Mirae Asset Financial Group, “seeks to harness the effects of changing consumer lifestyles by investing in companies geared toward promoting physical activity and well-being.”

The 64 companies in the fund are all listed on public stock exchanges, and so their financial metrics may differ from younger start-ups introducing innovative technologies, typically considered a high-risk-high-reward investment. However, analysing their revenue and EBITDA multiples allows us to establish a benchmark that can be useful to infer the valuation of a private company.

Health & Wellness Valuation Multiples

Predictably, the pandemic accelerated the growth in Revenue multiples for wellness companies, which saw a correction over the course of 2021, although maintaining an upwards trajectory overall.

Median Revenue multiples jumped 70% between Q1 2020 and Q1 2021 before dropping all throughout 2021 and for most of 2022. Multiples have been stagnating for the past couple of years: in Q4 2023 the median EV/Revenue multiple for Wellness & Health companies was 1.2x, only slightly under pre-pandemic levels.

Source: YCharts

It is useful in this case to compare these numbers with those of HealthTech and TeleHealth companies, which show higher revenue multiples (5.6x in the second half of 2021).

In our cohort, only companies in the top-25% achieve comparable results, with the highest revenue multiples throughout 2022 being between 10x and 15x.

Source: YCharts In the chart above, the lines indicate the range of EV/Revenue multiples in our cohorts, while the boxes highlight the Interquartile Range (IQR), which is where the median 50% of the cohort ranks based on their valuation multiple.

EV/EBITDA multiples an equivalent a correction post-pandemic, reaching their peak at 13.8x in Q2 2021 and then falling. In Q4 2023 the median EV/EBITDA multiple for Health & Wellness companies was 9.8x.

Source: YCharts

EBITDA multiples for Wellness are analogous to those of HealthTech companies (12.5x in H2 2021), showing that one of the main challenges for wellness is achieving a sufficient profit margin, which is probably easier for tech or software based services than it is for consumer product manufacturers.

EBITDA multiples also show a wider range than their Revenue counterparts, with the median 50% of companies recording multiples between 7x and 17x in the last quarter of 2023.

Source: YCharts In the chart above, the lines indicate the range of EV/EBITDA multiples in our cohorts, while the boxes highlight the Interquartile Range (IQR), which is where the median 50% of the cohort ranks based on their valuation multiple.

The information available on this page is of a general nature and is not intended to provide specific advice to any individuals or entities. We work hard to ensure this information is accurate at the time of publishing, although there is no guarantee that such information is accurate at the time you read this. We recommend individuals and companies seek professional advice on their circumstances and matters.

-

Lessons From The UK’s Top 50 Exits

12 November 2025

The most successful founders are those who build a company to be bought, not sold.

Report : Exit and Trends

-

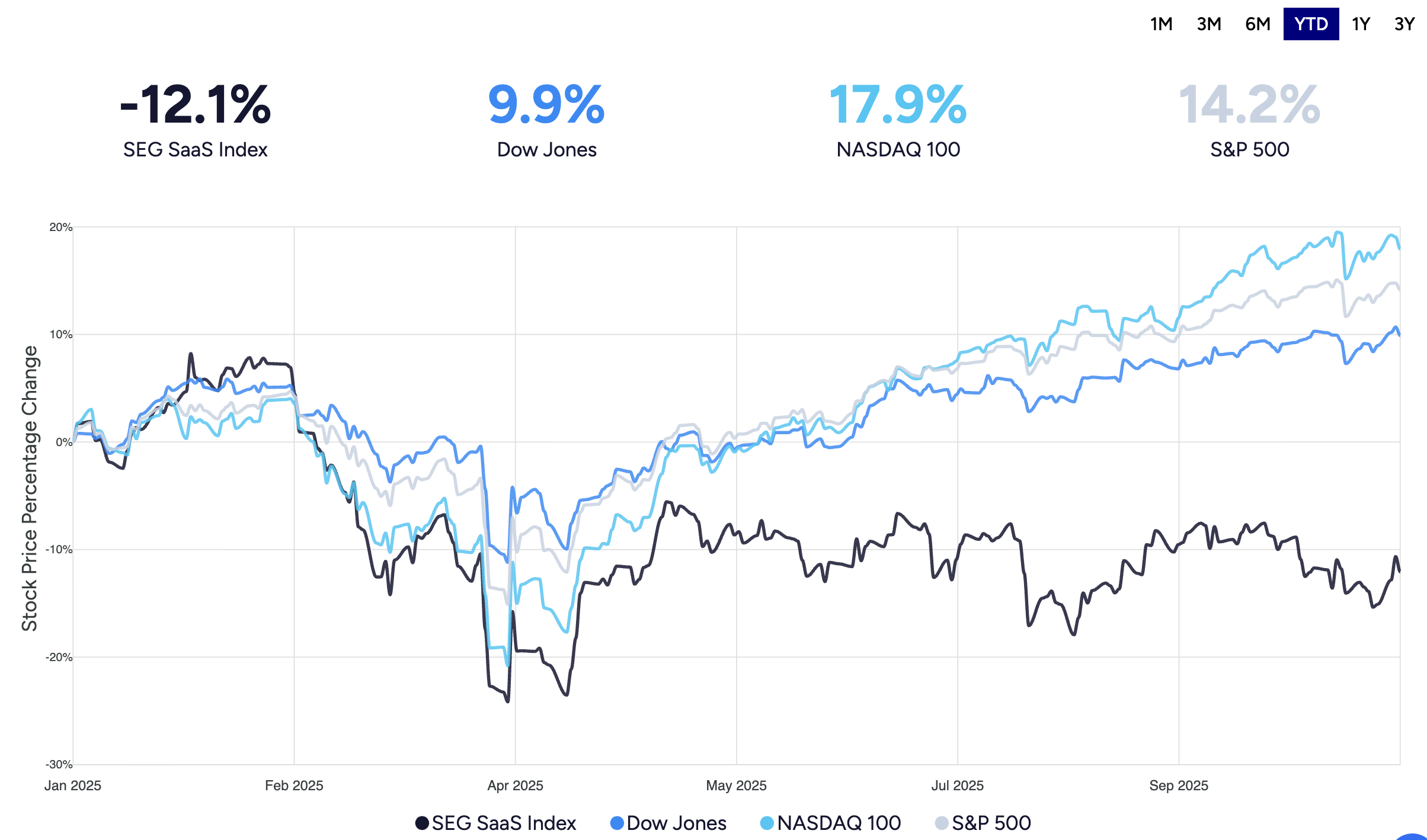

SaaS Stumbles in 2025: End of an Era, or Just Growing Pains?

23 October 2025

There is a widening gap between SaaS and the rest of the market starting in April 2025, and it’s just getting larger and larger.

Report : Tech and Valuation

-

The Jaguar Land Rover Cyber Attack: a £1.9bn Case Study in Systemic Risk

23 October 2025

The Jaguar Land Rover attack highlights several major threats and vulnerabilities in the cybersecurity space.

Report : Strategy and Trends

Sign up for the Founder's Bulletin

Join our community of 4,000 + Founders, Entrepreneurs & Advisors. Refreshingly simple financial insights to help your business soar.