EdTech: 2025 Valuation Multiples

The EdTech sector has been quietly developing since the dawn of the internet, pushed by increasing demand for digital learning solution, and occasionally boosted by external forces—most notably the pandemic. While the post-COVID landscape proved challenging for many EdTech companies that failed to keep their momentum going, the ubiquitous rise of AI might be about to fuel a new explosion for EdTech startups.

From distance learning to online subscription-based courses or language learning apps, most of us experienced some form of tech-enabled education since the COVID-19 pandemic.

Of course, the skyrocketing adoption of EdTech solutions during COVID meant a huge influx of investment into the sector, with companies growing and hiring aggressively and valuations and multiples on a steady upwards trajectory. However, once the pandemic was over, both the economic macro environment and this sector in particular faced completely different challenges, having to navigate a bearish market with scarce funding opportunities.

Out of the many EdTech companies that were quick at capitalising from the surge in demand during the pandemic, few had the stability to maintain their momentum. This hindered investors’ confidence in an already challenging market, causing many companies to announce layoffs or go bankrupt, although reports found that the European market proved more sturdy than the US or China.

Those who were able to consolidate the gains of 2020 and 2021, however, continued thriving. Coursera and Duolingo are often cited as examples of this, with the latter having had an incredible run in terms of both user growth and stock price in the past two years.

The use of generative AI to improve and create tailored and entertaining educational content is seen by many investors as a huge potential to boost the sector.

“Al holds the potential to promptly address learners’ needs, making it a game-changer. However, for Al to be truly transformative, educators must collaborate to ensure equitable practices and effective implementation,” said Vanessa Zurita, Director of District Impact at Digital Promise, in an interview with Forbes.

As we can see in some of the valuation multiple data from our research, the boom of AI may provide much-needed tailwinds for the EdTech sector.

In order to understand the trends reflecting the changing investor sentiment about companies in this space, we used The Global X Education ETF (EDUT), a fund managed by Mirae Asset Financial Group.

The fund “seeks to invest in companies providing products and services that facilitate education, including online learning and publishing educational content, as well as those involved in early childhood education, higher education, and professional education.”

Using financial data aggregator YCharts, we calculated distribution metrics for the funds’ companies’ valuations based on their revenue and profit metrics.

EdTech Valuation Multiples

Looking at revenue valuation multiples, we can see how—as a result of the pandemic—valuations for EdTech companies rose throughout 2020 and then faced a correction throughout 2021, before finally plummeting to about half their pre-pandemic levels by mid-2022.

Starting at 2.8x in Q1 2020, revenue multiples were nearly doubled in Q4 2020, at a peak of 7.2x. However, as schools reopened in most countries and the momentum around the sector came to an end, median revenue multiples fell all the way down to 1.5x by the third quarter of 2022. Although the end of 2023 showed a hint of an upwards trajectory, multiples have since stalled: the median revenue multiple for EdTech companies was 1.6x by Q4 2024.

Source: YCharts

The distribution chart below shows just how widespread the crisis has been in the EdTech sector, with the entirety of the sample faring below peak median levels, showing that even EdTech’s top player took a major hit in terms of their multiples and valuations. It will be interesting to see if the players in the cohort who are able to effectively harness AI tools will drive up the top quartile in the coming quarters.

Source: YCharts In the chart above, the lines indicate the range of EV/Revenue multiples in our cohorts, while the boxes highlight the Interquartile Range (IQR), which is where the median 50% of the cohort ranks based on their valuation multiple.

The trend for median EBITDA multiples—which track how valuations vary in relation to profit—is rather similar. After peaking at 26x in Q3 2021, EBITDA multiples fell by over 60% to a low of 8.1x in two years.

However, median EV/EBITDA multiples for EdTech companies shot up in the second half of 2023, and remained relatively high throughout last year, reaching 13.4x in Q4 2024. This underlines how companies that have a stable enough business model to drive in substantial profits are promptly rewarded by the investment market.

Source: YCharts

Differently from revenue multiples, some companies in EdTech managed to maintain relatively high profit multiples all throughout 2023 and 2024, with the top 25% of the sample recording EBITDA multiples between 20x and 60x at the end of last year. However, the remaining 75% of the sample is still well below the sector’s median at its peak.

Source: YCharts In the chart above, the lines indicate the range of EV/EBITDA multiples in our cohorts, while the boxes highlight the Interquartile Range (IQR), which is where the median 50% of the cohort ranks based on their valuation multiple.

The information available on this page is of a general nature and is not intended to provide specific advice to any individuals or entities. We work hard to ensure this information is accurate at the time of publishing, although there is no guarantee that such information is accurate at the time you read this. We recommend individuals and companies seek professional advice on their circumstances and matters.

-

Robotics & AI: 2026 Valuation Multiples

3 February 2026

Robotics & AI Companies started 2025 with a median EV/EBITDA multiple of 15.8x, dipping slightly in Q2 before rising to 16.8x in Q4 2025.

Report : Tech, Trends and Valuation

-

Lessons From The UK’s Top 50 Exits

12 November 2025

The most successful founders are those who build a company to be bought, not sold.

Report : Exit and Trends

-

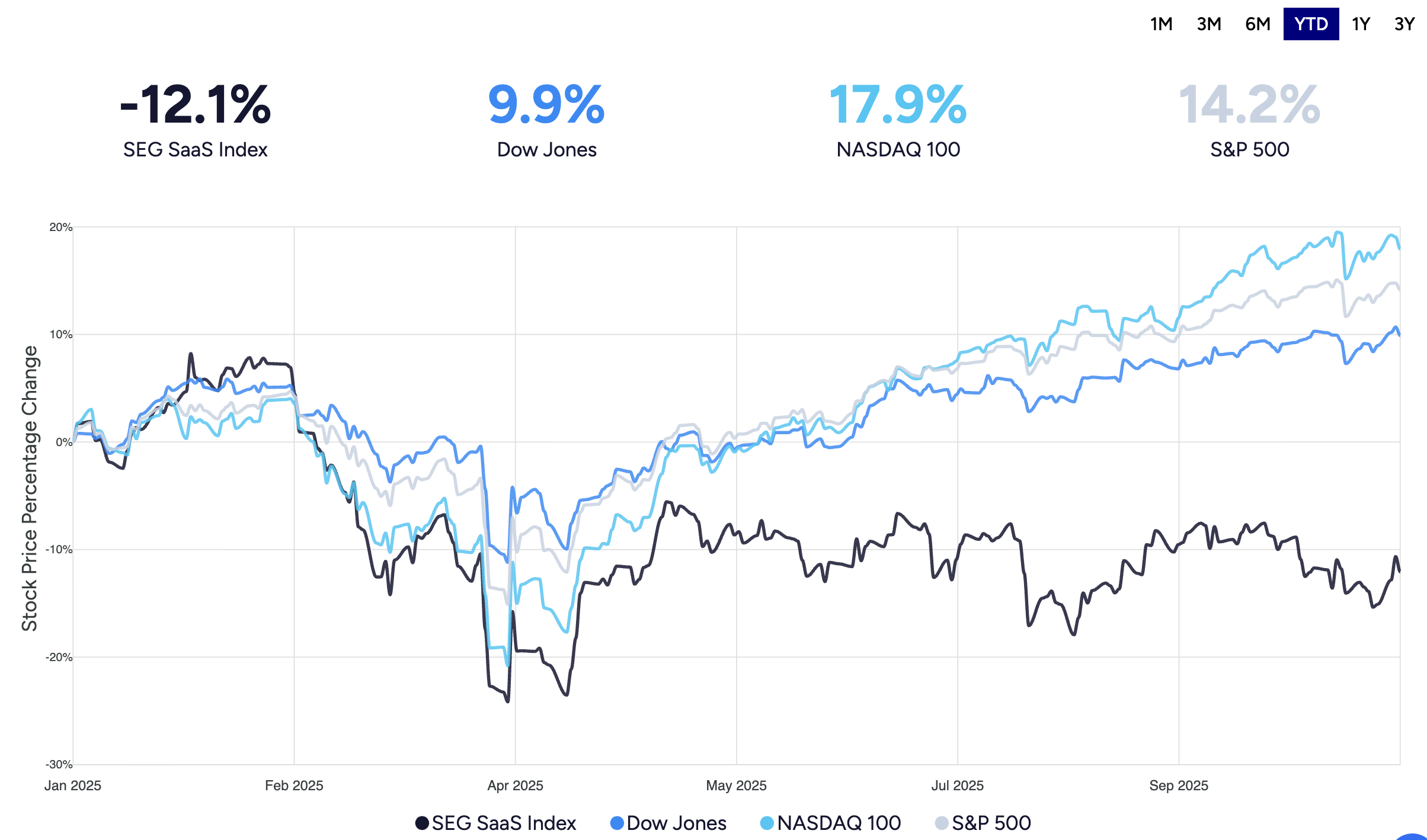

SaaS Stumbles in 2025: End of an Era, or Just Growing Pains?

23 October 2025

There is a widening gap between SaaS and the rest of the market starting in April 2025, and it’s just getting larger and larger.

Report : Tech and Valuation

Sign up for the Founder's Bulletin

Join our community of 4,000 + Founders, Entrepreneurs & Advisors. Refreshingly simple financial insights to help your business soar.