Beauhurst 2025 Funding Review: A Return to Form for Early-Stage Founders

For at least four years now, the UK equity market has been characterised by sustained caution from investors, especially when it comes to early-stage ventures, with the number of completed funding rounds declining steadily year on year, and only a few megadeals keeping average deal size figures afloat. However, according to The Deal 2026, the annual review from Beauhurst and Mercia Ventures, a first signal of a change in investor sentiment might emerge from last year’s data.

Here is our analysis of the key figures in the report and what they mean for founders raising in 2026.

First-Time Deals Rebound

The most compelling data point for early-stage ventures is the resurgence of first-time fundraises. After declining volumes in previous years, the number of UK companies securing their first funding round rose by 23.6% in 2025, reaching a total of 2,489 companies.

This increase in volume was matched by a significant rise in capital committed. The total amount invested in first-time deals reached £6.27 billion, a 74.3% increase year-on-year. This figure surpasses the previous post-pandemic peak of £5.70 billion recorded in 2021, bringing the average deal size for these first rounds has increased to £2.62 million.

This indicates that while the bar for entry remains high, investors are demonstrating higher conviction, backing new companies with larger initial cheques to help them reach scale faster.

Market Recalibration

Will Clark, Managing Director of Mercia Ventures, describes this shift not as a market retreat, but as a “refining” of focus.

The broader market statistics echo this sentiment. While the total number of deals across all stages dipped by 7.87% to 5,887, the total amount of capital deployed actually increased to £24.0 billion, up from £23.2 billion in 2024, a finding confirmed by multiple sources, such as HSBC’s UK Innovation Update.

As expected, AI remains the primary driver for this rebound, with capital deployed into AI companies rising by 62.6% to reach a record £7.70 billion. This sector alone accounted for nearly a third (32.0%) of all equity investment raised in the UK last year.

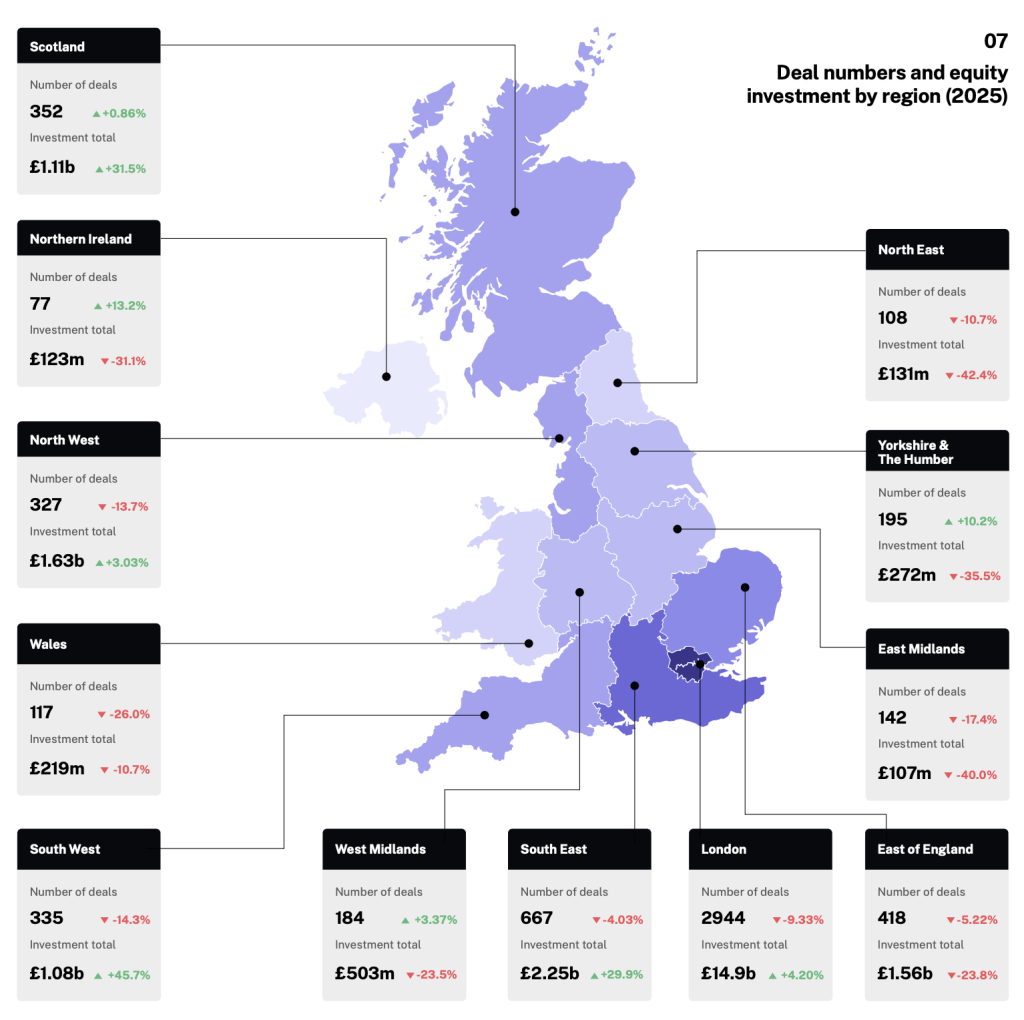

Regional growth data, on the other hand, showed an interesting picture of redistribution, with London unusually seeing declining number of deals and stationary amounts invested in favour of historically underrepresented regions such as Northern Ireland, Scotland and the South West of England.

Implications for Seed-Stage Founders

The data from 2025 suggests that the “funding winter” may be starting to thaw, particularly for new companies. However, the increase in average deal size alongside a dip in overall deal volume implies that competition for capital remains intense. Investors are deploying more money, but into fewer, higher-quality assets.

For founders preparing to raise in 2026, the focus should remain on the fundamentals that drove 2025’s activity: clear unit economics, defensible technology (particularly in AI and deep tech), and a validated path to growth.

The information available on this page is of a general nature and is not intended to provide specific advice to any individuals or entities. We work hard to ensure this information is accurate at the time of publishing, although there is no guarantee that such information is accurate at the time you read this. We recommend individuals and companies seek professional advice on their circumstances and matters.

-

Green Energy & Renewables: 2026 Valuation Multiples

6 April 2026

The outbreak of war in Iran and the broader Middle East in early 2026 has radically altered the global energy landscape, providing an unexpected boost to green energy valuations.

Report : Tech, Trends and Valuation

-

B2B SaaS: 2026 Valuation Multiples

25 February 2026

While B2B SaaS Revenue Multiples saw a slight recovery in 2024 to 6.7x, they contracted again in 2025, settling at 5.9x.

Report : Exit, Investment, Tech and Valuation

-

Robotics & AI: 2026 Valuation Multiples

3 February 2026

Robotics & AI Companies started 2025 with a median EV/EBITDA multiple of 15.8x, dipping slightly in Q2 before rising to 16.8x in Q4 2025.

Report : Tech, Trends and Valuation

Sign up for the Founder's Bulletin

Join our community of 4,000 + Founders, Entrepreneurs & Advisors. Refreshingly simple financial insights to help your business soar.